If you are a government entity that is a Transferor in a PPP arrangement, add the PPP contract in LeaseCrunch in the identical manner as a Lessor would under GASB 87 with the following three exceptions:

- Paragraph 14,21: The Operator makes improvements to the asset belonging to the Transferor. In this case, the Transferor, for the acquisition value, book a journal entry to debit an Asset and credit Deferred Inflow of Resources when the asset is placed in service. Amortize the Deferred Inflow of Resources into Revenue over the PPP Term. See options below for booking journal entries.

- Paragraph 15,18-20: The PPP asset is a new asset purchased or constructed by the Operator and the PPP meets the definition of an SCA. In this case, the Transferor, for the acquisition value, would book a journal entry to debit an Asset and credit Deferred Inflow of Resources when the asset is placed in service. Amortize the Deferred Inflow of Resources into Revenue over the PPP Term. See options below for booking journal entries.

- Paragraph 16, 31: The PPP asset is a new asset purchased or constructed by the Operator and the PPP does not meet the definition of an SCA, when the underlying PPP asset is placed into service. In this case, The Transferor, at the Operator’s estimated carrying value at the expected date of the transfer of ownership, would book a journal entry to debit a Receivable and credit Deferred Inflow of Resources when the asset is placed in service. Amortize the Deferred Inflow of Resources into Revenue over the PPP Term. See options below for booking journal entries.

Booking journal entries for the exceptions above can be done in the following manner:

Option 1: Make entries outside LeaseCrunch. The Revenue should be added to the Footnote export from LeaseCrunch.

Option 2:

- At Transition Date when setting up the PPP in LeaseCrunch: Go to Administration/GL Accounts/Existing Balances, select Lessor GL Accounts and create a new GL Account (select Liability Category) and use a GL Description such as “Asset-GASB 94” (or “Receivable-GASB 94” if under paragraphs 16,31). Add the value of the Asset (or Receivable) at Step 2 of Add Leases:

This creates the following entry:

Dr. Asset-GASB 94 10,000

Cr. Deferred Inflow of Resources 10,000

-

AFTER Transition Date when setting up the PPP in LeaseCrunch:

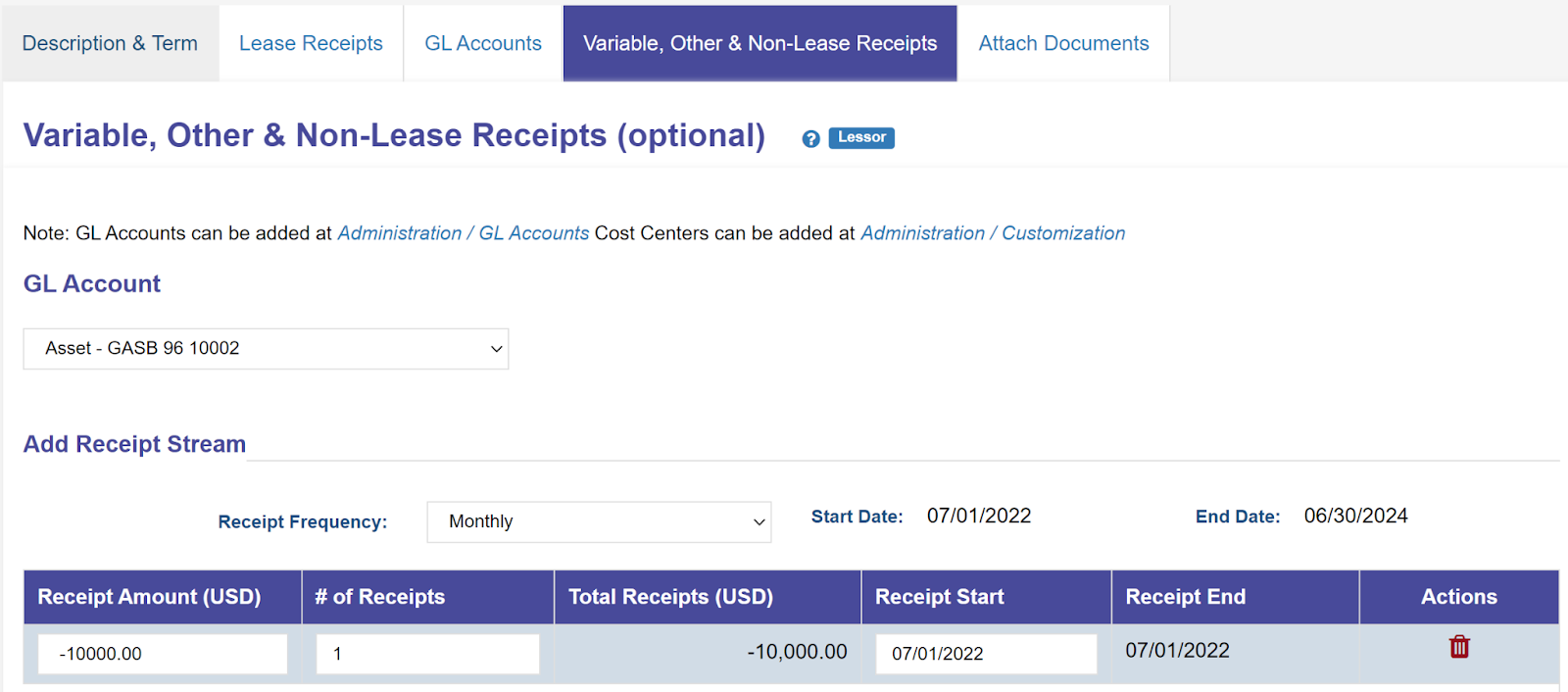

1) Go to Administration/GL Accounts/Variable & Non-Lease Receipts, select Lessor GL Accounts and create a new GL Account (select (Other Balance Sheet Category) and use a GL Description such as "Asset-GASB 94" (or "Receivable-GASB 94" if under paragraphs 16,31).

2) When adding the lease, add a Lease Receipt for the Asset (or Receivable) value before the start of the PPP Term:

-

This will create the following entry (Entry 1):

-

Dr. Cash/Clearing Account 10,000

-

Cr. Deferred Inflow of Resources 10,000

-

-

- 3) Also while adding the lease, in the "Variable, Other & Non-Lease Receipts" section, select the GL Account created in the first step and add a Negative Receipt for the same amount added in the "Receipts" section:

-

This creates the following Journal Entry (Entry 2):

-

Dr. Asset-GASB 94 (or Receivable if under paragraphs 16,31) 10,000

-

Cr. Clearing Account 10,000

-

-

- Note: The combination of Entry 1 & 2 eliminates the Cash/Clearing Account resulting in a debit to Asset (or Receivable) and a credit to Deferred inflow of Resources. The Deferred Inflow of Resources will be amortized into the Revenue over the Term without any additional steps by the user.

- Note 2: Per paragraphs 20, 21, the Asset-GASB 94 should be accounted for by applying other accounting and financial reporting requirements relevant to this PPP asset.