LeaseCrunch Blog

Read about ASC 842 & other lease accounting topics

There’s no two ways about it: Lease accounting can seem very confusing. But when you have experts at the helm who are able to explain the more complicated topics in a way that makes them easier to understand, everything becomes simpler.

In this blog, we took the concepts about which we get the most questions and provided examples and thorough walkthroughs of how to deal with them correctly and easily. We will cover things such as:

We begin by describing what ASC 842 requires for lease accounting, then we tackle the ins and outs of journal entries themselves, along with special cases and frequently asked questions.

The GAAP lease accounting standard ASC 842 requires all leases longer than 12 months to be recorded as assets and liabilities on balance sheets. The Financial Accounting Standards Board, or FASB, created this new standard to foster more transparency between companies and their financial statement users, who are typically investors or banks.

ASC 842 lease accounting replaces the previous GAAP lease accounting standard, ASC 840, which classified certain leases as “operating leases,” which were not capitalized on the balance sheet. As a result, they were excluded from many financial analysis ratios, such as the current ratio, and these exclusions could skew an investor’s understanding of a company’s performance.

Now, with the ASC 842 lease accounting standard, all organizations that follow generally accepted accounting principles, or GAAP, are required to classify leases as either finance leases or operating leases and record liabilities and right-of-use assets on the Balance Sheet.

Under the ASC 842 lease accounting standard, leases are classified as either: operating leases or finance leases. Operating leases are those where the terms do not mimic the purchase of an asset, while finance leases have characteristics that are similar to purchasing an underlying asset.

Every lease with a term longer than 12 months that falls under the accounting principles outlined by FASB is classified as either an operating or finance lease.

The examples below are identical leases in terms, payments, and discount rates. The only difference is lease classification. Isolating this variable can help you better understand the impact of ASC 842.

One thing that is important to remember is that the Lease Liability is the present value of future lease payments regardless of the the lease classification of finance or operating lease.

To show what ASC 842 journal entries would look like for operating leases, we are going to give an example.

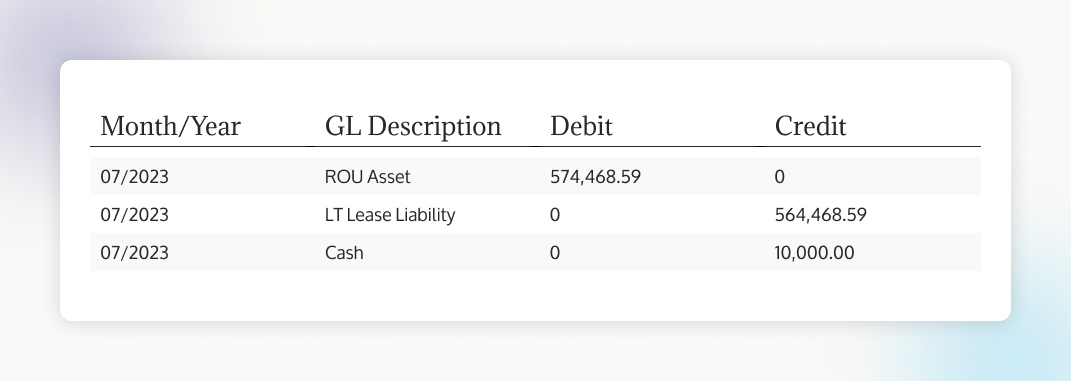

Suppose you have a 5-year lease beginning 7/1/23 through 6/30/28. The discount rate is 4.19% and the payments are $10,000 with a 3% annual increase, making the total lease payments over the course of the lease $637,096.32

Now, let’s break out the details of the entry:

Initial Recognition of the Lease Liability: $564,468.59

The lease liability is the present value of any future lease payments. Note that this amount does not include the first payment made, as it is not considered a future lease payment.

Initial Recognition of the ROU Asset: $574,568.59

The initial recognition of the ROU asset is the sum of:

Cash: $10,000

This is the cash outlay at commencement. Note that this is not a future payment and therefore not included in the lease liability.

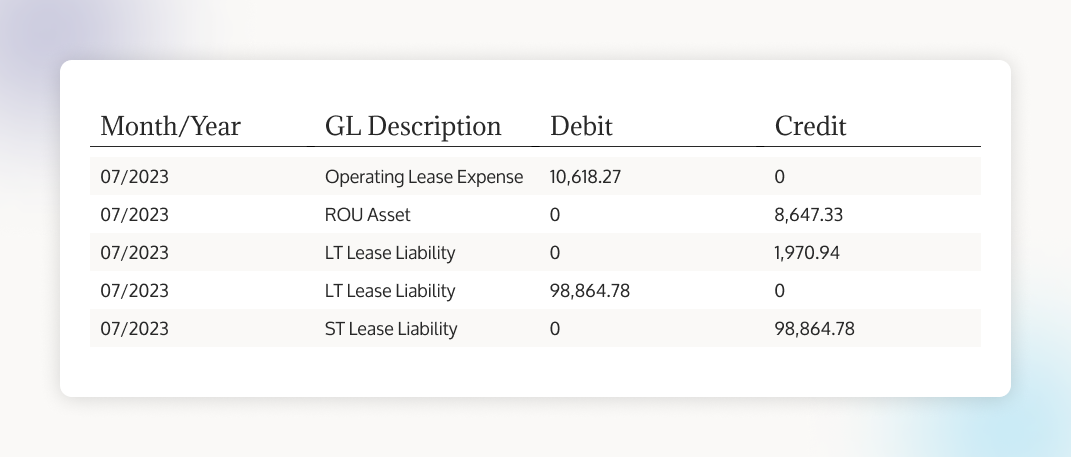

The subsequent recognition entry for the first month of the lease will resemble something like this and includes the adjustment to reclass short term lease liabilities.

Operating Lease Expense: $10,618.27

Operating lease expense calculations are unchanged from the previous standard. These calculations are a straight-line expense calculation that equals the sum of the lease payments divided by the ROU asset’s useful life (which is generally the same as the lease term). Because this is a straight-line expense calculation, it might not equal the lease payments.

ROU Asset: $8,647.33

The ROU asset reduction is the difference between the operating lease expense and the change in lease liability from the prior month. This amount is not the same from month to month since the lease liability reduces monthly, therefore the interest accrued is on a smaller amount through the life of the lease.

The lease liability is always the present value of future lease payments. Therefore, the monthly journal entry adjusts the lease liability balance to the current month’s present value of future lease payments.

Long-Term Lease Liability: $1,790.94

The increase in long-term lease liability is the interest accrued on the remaining liability. This amount is calculated using the discount rate divided by 12 (to determine the monthly rate) multiplied by the prior months ending total liability (both short and long-term liability are used, in this case) less any payment made at the beginning of the month.

Long-Term Lease Liability: $98,864.78

The decrease in long-term lease liability is the adjustment to record the amount of short-term liability due in the next 12 months.

Short-Term Lease Liability: $98,894.78

The amount of liability that is less than 12 months from this point in time.

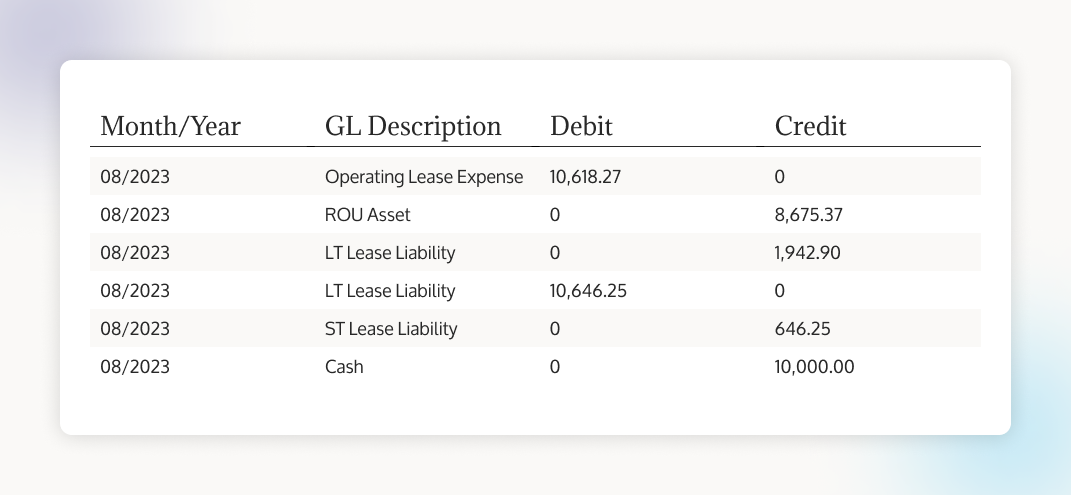

Further subsequent recognition after the first month of a lease will resemble the following:

Operating Lease Expense: $10,618.27

Operating lease expense is a straight line calculation similar to ASC 840. The operating lease expense is the sum of the lease payments divided by the useful life of the ROU asset (which is generally the same as the lease term). Because this is a straight-line expense calculation, it might not equal the lease payments and is consistent from month to month.

ROU Asset: $8,675.37

The ROU asset reduction is the straight line amortization of the ROU asset less the interest on the remaining lease liability. To calculate this, use the operating lease expense less the interest accrued on the remaining liability. This amount is not the same from month to month since the lease liability reduces monthly, therefore the interest accrued is on a smaller amount through the life of the lease.

Long-Term Lease Liability: $1,972.90

The increase in long-term lease liability is the interest accrued on the remaining liability. This amount is calculated using the discount rate divided by 12 (to determine the monthly rate) multiplied by the prior months ending total liability less any payment made.

Long-Term Lease Liability: $10,646.25

The decrease in long-term lease liability is the reduction of the lease payment’s long-term lease liability and the amount of short-term liability due in the next 12 months.

Short-Term Lease Liability: $646.25

This is a short-term lease liability adjustment to make sure the account remains showing the liability due in the next 12 months.

Cash: $10,000

This is the cash outlay for the lease payment during the period.

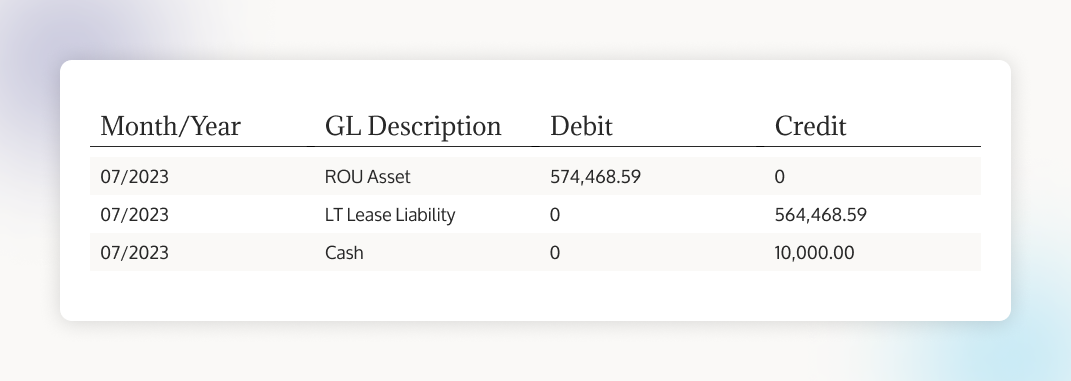

Here’s an example to show what ASC 842 journal entries would look like for finance leases.

Suppose you have a 5 year lease beginning 7/1/23 through 6/30/28. The discount rate is 4.19% and the payments are $10,000 with a 3% annual increase, making the total lease payments over the course of the lease $637,096.32.

For a Finance Lease, the initial ASC 842 journal entry will resemble this:

Let's break these out further.

Initial Recognition of the Liability: - $564,468.59

The lease liability is the present value of future lease payments. Note that this does not include the first payment made, as it’s not considered a future lease payment.

Initial Recognition of the ROU Asset: - $574,568.59

The initial recognition of the ROU asset is the sum of:

Cash: $10,000

This is the cash outlay at commencement. Note that this is not a future payment and therefore not included in the lease liability.

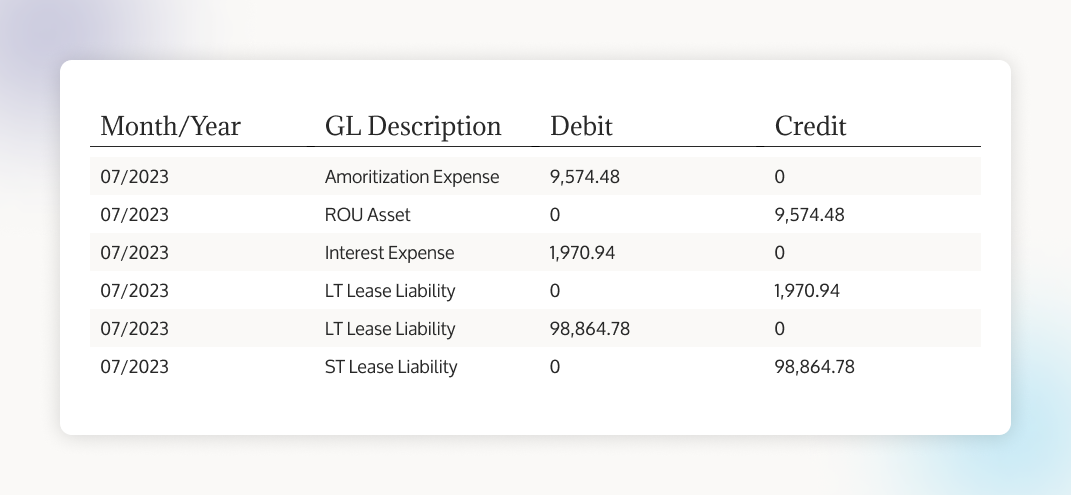

The subsequent recognition entry for the first month of the lease will resemble something like this and includes the adjustment to reclass short-term lease liabilities:

Amortization Expense: $9,574.48

Amortization expense is the straight line amortization of the ROU asset divided by the lease term.

ROU Asset: $9,574.48

This is a straight-line amortization of the ROU asset over the useful life of the asset divided by the lease term. This equals amortization expense.

Interest Expense: $1,970.94

This is the monthly Interest on the lease liability calculated as the discount rate divided by 12 (to determine the monthly rate) multiplied by the prior month's ending total liability, less any payments made.

Long-Term Lease Liability: $1,970.94

The increase in long-term lease liability is the interest accrued on the remaining liability. This amount is calculated using the discount rate divided by 12 (to determine the monthly rate) multiplied by the prior months ending total liability less any payment made.

Long-Term Lease Liability: $98,864.78

The decrease in long-term lease liability is the adjustment to record the amount of short term liability due in the next 12 months.

Short-Term Lease Liability: - $98,894.78

The amount of liability that is less than 12 months from this point in time.

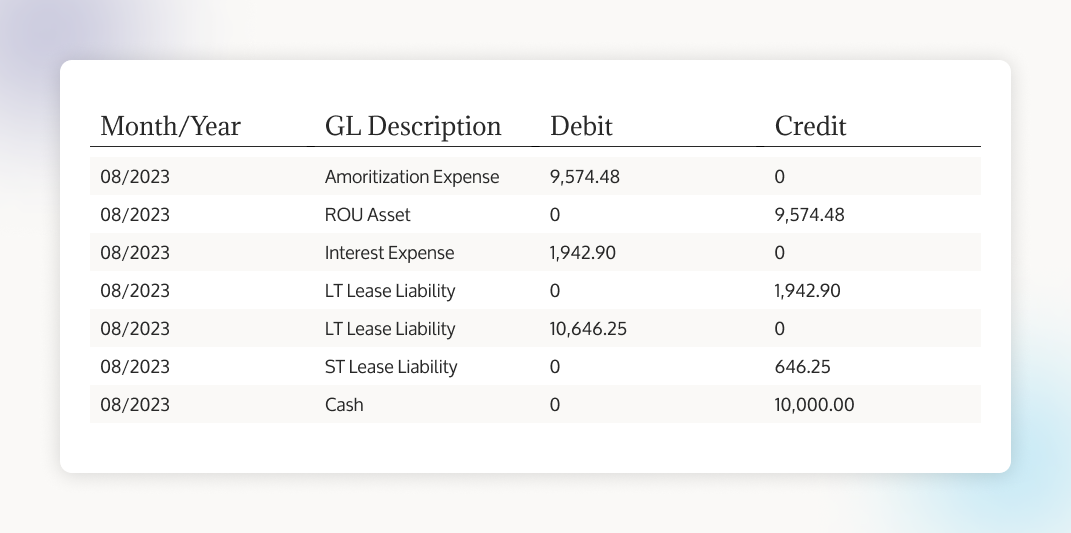

Further subsequent recognition after the first month of a lease will resemble the following:

Amortization Expense: $9,574.48

Amortization expense is the straight line amortization of the ROU asset divided by the lease term.

ROU Asset: $9,574.48

The ROU asset reduction is the straight line amortization of the ROU asset divided by the lease term. This equals the amortization expense.

Interest Expense: $1,942.90

This is the monthly Interest on the lease liability calculated as the discount rate divided by 12 (to determine the monthly rate) and multiplied by the prior month's ending total liability, less any payments made.

Long-Term Lease Liability: $1,942.90

The increase in long-term lease liability is the interest accrued on the remaining liability. This amount is calculated using the discount rate divided by 12 (to determine the monthly rate) multiplied by the prior months ending total liability less any payment made.

Long-Term Lease Liability: $10,646.25

The long-term lease liability is the reduction in the liability for the period. This is the cash payment plus the short-term lease liability for the period.

Short-Term Lease Liability: $646.25

This is the short-term lease liability adjustment to make sure the account remains showing the liability due in the next 12 months.

Cash: $10,000.00

This is the cash outlay for the lease payment during the period.

Now that we’ve covered the steps of how to complete the ASC 842 journal entries for both operating and finance leases, how do you record them? With easy-to-use lease accounting software readily available, most accountants prefer software over complicated and prone-to-error spreadsheets for their lease accounting calculations.

Avoid pitfalls altogether by using modern lease accounting software that is built to prevent mistakes and errors in your ASC 842 journal entries. To record ASC 842 journal entries for a lease while avoiding errors, we recommend investing in well-developed lease accounting software.

A sale-leaseback transaction is an asset transfer that occurs between an existing lessor, the seller; and a lessee, the buyer. When a sale-leaseback transaction occurs between a seller-lessee and a buyer-lessor, accounting for this type of transaction becomes more difficult.

In a successful sale-leaseback transaction, both the seller and buyer must determine if a purchase has occurred, apply Topic 606 to determine if a contract exists, and make sure that control of the asset has been transferred. Furthermore, there must be a contract between the parties and transfer of the underlying asset to the buyer-lessor has to satisfy performance obligations (see Topic 606).

Organizations may opt into sale-leaseback transactions to increase cash flow without increasing debt. Organizations that opted into the transition relief package of three practical expedients and did not reclassify their leases did not need to account for existing sale-leasebacks differently under ASC 842 than they had under ASC 840.

For new sale-leaseback transactions, the guidance has changed, and organizations will first determine if there is a contract (sale) under Topic 606-10-25-1 through Topic 606-10-25-8 before accounting for the transaction. When it is determined that there is a sale, the entity must decide if the performance obligation has been met and if control of the asset has been transferred. Under ASC 842, both the seller-lessee and the buyer-lessor must separately determine if control of the asset is transferred. It is also important that the seller-lessee and buyer-lessor use the same lease classification. If they do not, then control has not been transferred and the transaction is accounted for as a financing transaction.

Once it has been determined that a transaction is eligible for sale-leaseback accounting, the seller-lessee will determine if the transaction is at fair value based on the difference between either the sale price of the asset and the fair value of the asset, or the present value of lease payments and the present value of market rent payments. The seller-lessee should use whichever is more readily determinable.

If the transaction is not at fair value, the seller-lessee will adjust the sale price of the asset on the same basis used to determine the transaction was not at fair value. The seller-lessee will recognize the sale and any gain or loss associated with the sale of the asset and the buyer-lessor will record a purchase. The seller-lessee will de-recognize the asset and record the ROU asset and lease liability in accordance with the lease details. The buyer-lessor will account for the purchase of the underlying asset as it would other nonfinancial assets and account for the leaseback under ASC 842 lessor accounting.

When a seller-lessee or buyer-lessor enters into a sale leaseback transaction, they should provide disclosures similar to those required by ASC 842-20-50-1 through 9 and ASC 842-30-50-1 through 13, respectively. In addition, the seller-lessee should include the main terms and conditions of the transaction and any gain or loss resulting from the transaction separately from other gains or losses from disposal of other assets.

Incentives can be either the payments made by the lessor to the lessee, or the reimbursement or assumption of costs of a lessee by a lessor. Often, a lessor may offer to assume the payments from a lessee’s pre-existing lease with a third party. At commencement, lease incentives are treated as a reduction of the ROU asset when they are paid or payable.

An example of a lease incentive would be a potential lessee that has three months remaining on their current lease, but a prospective lessor wants them to move to their building early, so this new lessor offers to pay the lessee’s remaining rent. This incentive reduces the ROU asset at commencement of the new lease.

It’s common for lessors to offer incentives to lessees that are payable after commencement and contingent on future events. When incentives are paid after the lease commencement and the lessee is reasonably certain the payment will be received, we believe the lease liability should be reduced by recording a negative lease payment or payments at the time the incentive is expected to be received. If, after commencement, the timing of the incentive payment changes from the originally expected timing, the lessee would follow remeasurement guidance using the discount rate and classification immediately prior to the remeasurement date.

As with other amounts included as lease payments, incentives are included as part of allocating consideration in the contract when multiple components exist.

Equity is very rarely affected under ASC 842, as everything flows through the ROU asset—including deferred rent. With that said, the following items do have the potential to affect equity:

Under GASB 87, a lessee is required to recognize both a lease liability and a lease asset at commencement of a lease term. That lease liability, similar to ASC 842, is the present value of future lease payments. The lease assets are then measured as the initial amount of lease liability plus any payments made to the lessor at or before the time of the commencement of the lease and less any incentives received from the lessor.

A lessor is required to recognize a lease receivable and a deferred inflow of resources. The lease receivable is measured as the present value of lease receipts expected through the term, and deferred inflow of resources are measured as the lease receivable adjusted for prepayments or incentives paid.

The steps to account for a lessee lease under GASB 87 are as follows:

GASB 96 introduced the notion of a “SBITA,” or a subscription-based information technology arrangement. A SBITA is a contractual agreement between a government and an IT vendor that allows the government to use the IT Vendor’s software for a predetermined period of time.

SBITAs should be accounted for in a similar manner to leases under GASB 87. When a government entity enters into a SBITA, they recognize the subscription asset and a related subscription liability on financial statements. The value of these is determined by calculating the present value of subscription payments that are due over the term of the SBITA and discounted by a discount rate. The government entity should then amortize these assets in a systematic and rational manner over the subscription term, thereby further reducing the subscription liability caused by payments made during the term.

If you need help adding a SBITA in your LeaseCrunch accounting software, check this Knowledge Base page out.

Although ASC 842 has been in effect for quite some time now, lease accounting can still prove tricky sometimes, especially when you’re accounting for a number of different leases. Specialized, customizable software solutions, designed by CPAs from top accounting firms, come in handy when you want to increase the efficiency of your lease accounting process while not sacrificing accuracy.

Our lease accounting software has the processing power and security you would expect from a large firm, with the hands-on, white glove experience one would get from a boutique accounting service. LeaseCrunch is used by government entities, CPA firms, and auditors because of its:

Interested in trying LeaseCrunch or have any lingering questions? Don’t hesitate to reach out. Contact us today!

What Is ASC 842?

ASC 842 is a lease accounting standard promulgated by the Financial Accounting Standards Board (FASB). It requires all leases longer than 12 months to be reflected on a company's balance sheet. This enhances financial transparency by giving a clear picture of an entity's committed future payment obligations.

What Is the ASC 842 Implementation Process?

The ASC 842 implementation process involves a series of steps starting with identifying leases and gathering all of an entity's relevant leased assets. The key lease terms are then extracted and subsequently classified as finance or operating leases and are used in calculating the right-of-use (ROU) assets and lease liabilities which are reported on the balance sheet.

Is ASC 842 Part of GAAP?

Yes, ASC 842, also known as the new lease accounting standard, is part of the Generally Accepted Accounting Principles (GAAP). It significantly changes how companies account for operating leases and contributes to the transparency of lease obligations on financial statements.

How Many ASC Standards Are There?

There are around 90 generally accepted accounting principles (GAAP) that have been released and recognized by the FASB. You can browse the FASB Codification list here and view any GAAP lease accounting standard you’d like.

What Is ASC U.S. GAAP?

ASC stands for accounting standards codification, and GAAP stands for generally accepted accounting principles. The ASC U.S. GAAPs are a set of accounting standards released and maintained by the Financial Accounting Standards Board.

Is ASC 842 Mandatory?

The ASC 842 lease accounting standard is mandatory for all private companies and nonprofit organizations that follow GAAP and have leases longer than 12 months.

Is IFRS the Same as ASC 842?

When it comes to operating leases under IFRS 16 and ASC 842, they diverge in intent and effect. Under IFRS 16, there are only finance leases—the International Accounting Standards Board eliminated the concept of the operating lease. In the U.S. under ASC 842 lease accounting, organizations still need to classify leases as either operating or finance leases. Despite this difference, both require all leases over 12 months in length to be recorded on the balance sheet.

What Is the FASB Codification System?

The FASB codification system is the source of authoritative GAAPs recognized by the FASB to be correct and true.

What Leases Are Subject to ASC 842?

For organizations that follow GAAP, all leases 12 months and longer need to adhere to the accounting standards in ASC 842.

How Is ASC 842 Implemented?

Implementing ASC 842 is complicated. We recommend checking out this guide, reviewing this list of mistakes to avoid, or considering investing in lease accounting software that stays automatically compliant.

How Do I Record a Lease Under ASC 842?

Under ASC 842, all leases 12 months and longer must be identified on the balance sheet. Furthermore, both the lessor and lessee are required to identify these leases.

Does ASC 842 Affect Income Statements?

ASC 842 lease accounting will generally have a minimal impact on a lessee’s income statement.

What Entities Must Comply With ASC 842?

All entities that follow GAAP and have leases longer than 12 months in length must comply with the rules stated in the ASC 842 lease accounting standard.

How Does ASC 842 Handle Lease Modifications?

In some cases, if a lease is modified, a lessee should recalculate the ROU asset and the lease liability.

Can Short-Term Leases be Excluded from Capitalization Under ASC 842?

All leases must be capitalized under ASC 842 except for those that are less than 12 months in length if a policy election is made.

How Does ASC 842 Affect EBITDA?

Since ASC 842 didn’t change income statements, EBITDA isn’t really affected by this new lease accounting standard.

How Does ASC 842 Affect Lessor Accounting?

Under ASC 842, lessor accounting did not change as drastically as it did for lessees.